Can You Afford to buy a home in NYC in 2025?

Go Back To Previous PageWe determine if you can afford a home in NYC by deciding where you want to buy. Then, you figure out what mortgage you’ll  qualify for. Here’s what you’ll need to know about the NYC real estate market. This works for first-time home buyers or savvy investors.

qualify for. Here’s what you’ll need to know about the NYC real estate market. This works for first-time home buyers or savvy investors.

Buying a home in NYC isn’t as straightforward as in other parts of the country, and you can’t just determine what type of mortgage you’ll qualify for. Instead, you have to consider various factors, starting with the kind of property you’re buying.

For example, you might be able to afford a more expensive house in Brooklyn compared to a similarly priced co-op in Manhattan, and this is only because off the building’s policies. Here’s how to determine how much you can afford to buy a home in NYC.

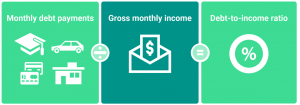

Start by calculating your debt-to-income ratio (“DTI”)

Your debt-to-income ratio, or DTI, helps illustrate the amount of debt you can afford to carry every month. The debt part of the equation includes housing costs like mortgage payments, property taxes, and insurance.

equation includes housing costs like mortgage payments, property taxes, and insurance.

You must also add other obligations such as credit cards, car payments, student loans, alimony, child support, and legal judgments. Additionally, the calculation does not include standard living costs like utilities and groceries.

The income part of the equation includes your salary and investment income. Depending on the lender, any income that may fluctuate, such as performance bonuses, may also be included.

To calculate your debt-to-income ratio, all you need to do is to divide your monthly debt obligations by your monthly income. For example, if your monthly debt totals $3,000 and your monthly earned income is $10,000. Then your debt-to-income ratio is around 30%.

Using DTI to calculate How many mortgages You Can Afford in NYC

You can use your debt-to-income ratio to calculate how much mortgage you can afford. This is before you know exactly how much your monthly mortgage payments (principal and interest) will be. DTI plays a significant role in getting approved for a mortgage, along with the credit score.

mortgage payments (principal and interest) will be. DTI plays a significant role in getting approved for a mortgage, along with the credit score.

Most lenders use a maximum DTI ratio of 43%. To calculate how much mortgage you can afford in NYC, multiply your income by 0.43 and subtract your non-housing liabilities. This rule also applies to home construction mortgages.

For example, if your income is $10,000 per month, you’d multiply that by 0.43, getting $4,300, from which you’d subtract your other debts. Let’s say they total $900. In that case, you could afford $3,400 in monthly housing costs. That doesn’t necessarily mean you can qualify for a $3,400 mortgage, though, as you still need to account for monthly carrying costs like standard charges, taxes, and insurance, among other things.

You can run this calculation with a simple mortgage calculator.

There’s no hard and fast rule for carrying costs.

Your monthly carrying costs will depend on the type of property you’re buying and other factors like the building’s financials. You’ll want to  work with your broker and mortgage lender to better understand your monthly carrying costs, as they could play a key role in determining how much you can afford to spend on your mortgage.

work with your broker and mortgage lender to better understand your monthly carrying costs, as they could play a key role in determining how much you can afford to spend on your mortgage.

Some apartments in buildings with ground leases might seem unusually affordable regarding home price or mortgage payment. Still, the monthly maintenance fees will be far higher than those of comparable properties that might cost more.

NYC Co-op Apartments Have Higher DTI Requirements

Your debt-to-income ratio will matter to your lender and the co-op board. If you plan on purchasing a co-op, you may encounter stricter DTI requirements, typically around 25-30%.

That means you’re better off calculating what you can afford based on the property’s requirements. If you plan on buying a house in Brooklyn or Queens, you can use the higher DTI the lender uses. However, if you’re purchasing a Manhattan co-op, you won’t be able to afford as much.

An experienced real estate professional will be an excellent asset, as they can leverage their expertise to help you find a home that best fits your budget and needs.

Calculate Your Down Payment

Once you know how much of a mortgage payment you can afford, you’ll need to ensure you can afford the down payment. While 20% down used to  be typical for most homes, you may find some NYC condos requiring only 10% down. On the other hand, co-ops have notoriously stringent requirements.

be typical for most homes, you may find some NYC condos requiring only 10% down. On the other hand, co-ops have notoriously stringent requirements.

It’s typical to see down payment requirements in the 20-30% range for co-ops, but some buildings require even higher amounts, up to 50%. A few select buildings also only accept all-cash buyers.

Don’t Forget About Closing Costs.

When you buy an apartment in NYC, you’ll be responsible for paying various taxes and fees. They include the mortgage recording tax, mansion tax, and transfer tax (for new developments). These fees associated with your purchase are called closing costs and will typically cost thousands of dollars.

Buyer closing costs vary depending on the type of property you’re buying but generally come to 2 to 4 percent of the property purchase price. These can be higher for new developments, as you’ll typically have to pay transfer taxes when buying a sponsor unit.

You might also need reserve funds or post-closing liquidity to buy a home.

Many co-op boards will want to ensure you can withstand any unexpected financial hardship. That means they’ll expect you to have additional cash on hand. A rule of thumb is to show at least two years’ worth of housing expenses in cash.

hand. A rule of thumb is to show at least two years’ worth of housing expenses in cash.

If you own any other investments, such as stocks or bonds, you may be able to use those as well.

The Takeaway: What you can afford to buy a home in NYC

It’s relatively straightforward to figure out how high a mortgage you can afford in New York City. However, it’s a lot trickier to navigate the market. This is where working with an experienced broker like NestApple will be invaluable.

We’ll help you better understand what you can afford to buy a home in NYC and where your money goes most while saving you thousands with a buyer commission rebate.

Georges has been working in Wall Street for the last 16 years trading derivatives with hedge funds. He has been an active real estate investor for over a decade. Georges graduated from HEC Business School in Paris and holds a master in Finance from ESADE Barcelona.