Can a Co-Signer or Guarantor Help You Get a Mortgage (2021)

Go Back To Previous PageMany people dream of buying a co-op or condo in New York City. However, it’s a pipe dream because they know they can’t qualify for a mortgage. They may have a low income, bad credit, or no savings, to name a few. But did you know that someone facing financial difficulties can still qualify for a mortgage? They can reach out to a Co-Signer or Guarantor in New York. A Co-Signer or Guarantor in New York can help you secure a mortgage. Then, your dream of owning a condo or a co-op may come true.

qualify for a mortgage. They may have a low income, bad credit, or no savings, to name a few. But did you know that someone facing financial difficulties can still qualify for a mortgage? They can reach out to a Co-Signer or Guarantor in New York. A Co-Signer or Guarantor in New York can help you secure a mortgage. Then, your dream of owning a condo or a co-op may come true.

If you have no credit history on favorable terms or no credit profile, seeking financial help will boost your chances of acquiring a loan. That’s why people combine forces with a Co-Signer or a Guarantor in New York. So what is a Co-Signer or Guarantor in New York?

And can they help you get a mortgage in New York? We’ve got you covered. If you want to buy a condo or co-op, read about borrowing a loan with someone else.

What is a Mortgage Co-Signer in New York real estate?

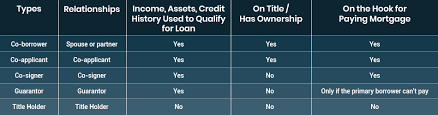

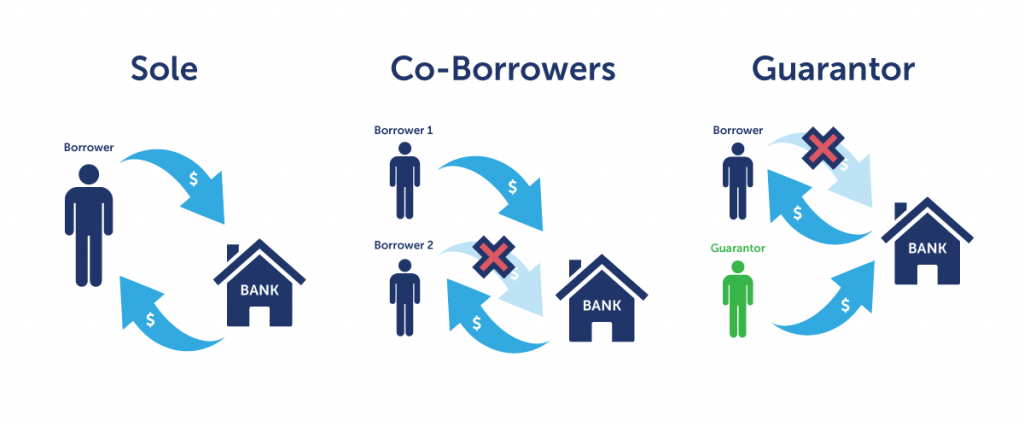

A co-signer can help you qualify for a home mortgage or seller financing when you have a low or bad credit score, limited finances, or a high debt-to-income ratio. A co-signer is a “co-borrower” or “co-applicant.”

limited finances, or a high debt-to-income ratio. A co-signer is a “co-borrower” or “co-applicant.”

The co-signer will take out a mortgage with the borrower and be listed as an additional borrower. Therefore, the co-signer’s income, assets, and credit history are considered to secure the loan. The co-signer must have an excellent credit score, a high income, and few or no financial blemishes throughout the years. In short, the co-signer lends their good name and credit history to help the buyer secure a loan.

The borrower and the co-signer will eventually jointly own the co-op or condo. Both their names will appear on the property’s title. The borrower is responsible for paying the mortgage. However, since their name is on the title, the co-signer is equally liable for making the loan’s monthly payments.

But there is a distinction.

The mortgage lender typically receives payments from the borrower, and the co-signer only comes in when the borrower fails to make a payment. This distinction is essential because the co-signer is responsible for paying if the borrower defaults.

make a payment. This distinction is essential because the co-signer is responsible for paying if the borrower defaults.

A co-signer, then, is a backup for the lender and a security measure. It lets the lender know that the loan gets paid without resorting to extraordinary measures.

For example, suppose the borrower has stopped making payments for any reason. In that case, the co-signer may have to cover the missed costs and penalties, such as late fees, additional interest, and more. As a result, becoming a co-signer is always a risk.

Who is the Co-Signer of a loan in New York?

The co-signer is sometimes a family member, relative, or friend unrelated to the borrower. However, the co-signer is usually the spouse or a romantic partner of the primary borrower. The lender refers to the co-signer who is not married to the borrower as the “co-applicant.” The lender issues individual loan applications for the same mortgage.

Therefore, the lender considers both the borrower and co-signer as independent entities with separate finances. However, if the co-signer is the borrower’s spouse, the two will complete only one mortgage application form together.

The co-signer does not have to live with the borrower in the apartment they jointly own. They can live elsewhere even if their name is on the mortgage or deed. Also, co-signers don’t need to be on the deed, but both names remain permanently on the borrower’s mortgage.

Co-signers are not required to qualify for a mortgage if the borrowers have enough funds to take on the loan themselves. However, the co-signer and borrower can still work together to afford a larger mortgage with lower interest rates.

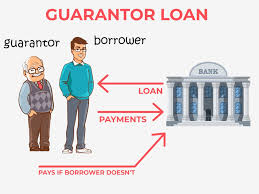

What is a mortgage Guarantor in New York real estate?

A guarantor is similar to a cosigner, as they help out the borrower. In a nutshell, a guarantor guarantees mortgage payments to facilitate mortgage approval. Unlike borrowers who need co-signers’ assistance, guarantors may have the finances to carry a mortgage independently but have difficulties securing a loan.

payments to facilitate mortgage approval. Unlike borrowers who need co-signers’ assistance, guarantors may have the finances to carry a mortgage independently but have difficulties securing a loan.

Maybe they have a low credit score or have significant credit issues.

Difference Between a Mortgage Co-Signer and mortgage Guarantor in New York

There’s a difference between a Co-Signer and a Guarantor in New York. Guarantors don’t have the same property rights as co- signers since their name is only on the mortgage and not the property title. The guarantor helps get mortgage approval and guarantees mortgage payments.

signers since their name is only on the mortgage and not the property title. The guarantor helps get mortgage approval and guarantees mortgage payments.

But there is an important distinction to make.

- Co-signers are answerable for the mortgage in the same way a borrower is. The co-signer is obligated to make monthly payments on the loan, not only the borrower’s responsibility.

- In contrast, guarantors are only responsible for the mortgage if they can’t make or have missed payments. Unlike a co-signer, the guarantor becomes liable for the loan if the primary borrower temporarily falls behind on payments.

This only happens after the lender has exhausted all other means of collecting payment from the borrower. However, a guarantor, unlike a cosigner, is not obligated to make monthly payments on the loan. It is only the borrower’s responsibility.

A guarantor is less risky.

The guarantor is only there to lend their good name to help the borrower close on the mortgage. But like the co-signer, the guarantor must also have good credit. In essence, the guarantor takes less risk when helping out a borrower. The guarantor is only responsible when the borrower defaults.

guarantor must also have good credit. In essence, the guarantor takes less risk when helping out a borrower. The guarantor is only responsible when the borrower defaults.

In contrast, the co-signer assumes greater risk when taking on additional financial responsibility. They are also in a better situation because they don’t own any part of the home. They are helping the borrower out of compassion, like a parent helping out an adult child.

Suppose guarantors want to reduce their financial responsibility, or significantly reduce it, to avoid becoming involved after securing the loan with the borrower. They can get the mortgage lender on board to open an interest-bearing savings account and deposit a one-time lump sum.

If the mortgage value decreases—usually to around 80% — the lender will release the guarantor from the agreement and refund the money.

What are the Risks of a Co-Signer in New York?

The co-signer must provide the lender with their credit history, credit score, income, debts, employment, and other financial information as part of the application. Borrowers can’t secure a loan independently because lenders rely on co-signers to increase the borrowers’ chances of qualifying. For this purpose, lenders pull hard inquiries on the co-signers’ credit as part of the loan application.

Hurts the FICO

The co-signer must proceed cautiously, as their credit score will be affected by the scoring models. So, serving as a co-signer for a borrower can hurt the co-signer’s credit. The mortgage will show on the co-signer’s credit report, and, as discussed, the co-signer is legally responsible for making payments on the loan if the borrower defaults.

Sometimes, the co-signer plans to apply for a home mortgage or a loan to purchase a vehicle or another expensive item. They may have difficulty securing such loans because the borrower’s loan shows up on the co-signer’s credit report. Conversely, if borrowers consistently make on-time payments on the loan, being a cosigner can help improve their credit scores.

Can a Mortgage Co-Signer Get Out of a Loan?

Yes, and it’s informally called a co-signer release. If the borrower fails to make payments on the loan or falls behind, the co-signer can request the co-signer’s release. It can only occur if two things happen:

- the borrower agrees to that condition and

- At the same time, he can demonstrate to the lender that he can make timely payments on the loan.

Are There Additional Risks of Being a Guarantor in New York?

Besides the financial risk, there is the relationship risk. The guarantor works with the borrower to help and may care about the borrower. For example, parents may wish to assist their adult child, and money is the ultimate gift they can give.

The risk here is that this gift or loan can ruin the relationship between the parent and the child. The parent may have second thoughts about becoming a guarantor if the adult child is not grateful. Another example is if the parent sees the child wasting money on foolish things.

The guarantor can mitigate this problem by scrutinizing the borrower’s finances before providing assistance. The guarantor should act as a loan officer to determine if the borrower is sincere and has the ability and willingness to pay the mortgage loan each month on his or her own.

The default of the borrower

As with a co-signer, the guarantor is also at risk, as their credit score will decline if the borrower defaults. As a result, it is difficult for the guarantor to secure a loan in the future. The guarantor usually assumes that the lender will go after the borrower if that borrower fails to make payments, and only after exhausting all options to reach out to the borrower.

However, lenders have the legal right to pursue the guarantor before contacting the borrower if they believe pursuing the borrower would be futile.

The guarantor will then pay for missed payments or the remaining loan amount. If the guarantor fails to pay, the latter is in default. But if the borrower is trustworthy and continues to make on-time, full payments on the loan, the guarantor will not be affected in any way.

Then, the guarantor’s credit rating won’t take a hit. The guarantor should still be ready to cover the loan if the borrower defaults, with sufficient funds to do so.

Can a Guarantor Get Out of a Loan?

There are reasons a guarantor might want to relinquish their role if they intend to take out a loan to buy a new home.

Suppose the borrower can find another guarantor or develop additional finances (such as getting a new job that pays more than their previous position). In that case, the lender will allow the guarantor to withdraw from the transaction. But even if there’s a new guarantor in place, it’s essential to know that the lender can disallow the switch at the lender’s discretion. The original guarantor gets stuck in the relationship with the borrower.

The guarantor can also put a safety net in place for the guarantor if the borrower defaults. The guarantor can open an interest-bearing savings account with a lender and deposit a lump-sum amount. When the mortgage’s loan-to-value decreases (usually to around 80%), the lender will release the guarantor from the loan agreement and refund the money.

Last Words of Wisdom

A Co-Signer or Guarantor in New York can help you qualify for a loan if you have insufficient funds or other risky financial obligations. Or, they can help you secure a larger loan or a lower interest rate. A co-signer is similar to a guarantor in that they agree to repay the loan if you can’t. Both give lenders peace of mind when extending your mortgage.

financial obligations. Or, they can help you secure a larger loan or a lower interest rate. A co-signer is similar to a guarantor in that they agree to repay the loan if you can’t. Both give lenders peace of mind when extending your mortgage.

It should be the last resort to seek help. Many risks are posed to the person who helps you. Why put someone in financial danger when you can wait?